Regarding the benefits that will arise from the type of agreement, there are several that we will deal with separately: order and make viable the profile of external payments (relaxation of the external restriction), monetary normalization and intertemporal fiscal sustainability, allow continuous growth with greater employment and improvement in social indicators, contributing in turn to consolidate a credible path of reduction in inflation.

In this note we will deal only with the first, which is to order and make the payment profile viable, improving the external restriction.

The six fronts of indebtedness

During the first two years of the MA, Argentina’s external indebtedness was stimulated in all its dimensions. Not only did the debt of the National Government increase, the external debt of the Provinces also grew (with the PBA as the leader) and the external commercial and financial indebtedness of private companies was encouraged. Finally, an insane innovation by that government, the holding of LEBACs and other debt in pesos by foreign creditors, including large hedge funds, was encouraged.

All these dollar inflows increased the BCRA Reserves and no one bothered to do the accounts that are done today. They were accounted for as net and liquid reserves. With these revenues, the real exchange rate appreciated, which typically inflates a country’s GDP in dollars and makes the Foreign Debt/GDP ratio seem sustainable. The unattended alarm was the current account deficit that reached 5% and the absence of productive investments.

This fantasy began to crack in mid-2018. At that time the perception of financial agents changed. Some residents and non-residents acted quickly and got out, While others were capped in 2019. To allow the exit, the debt taken was not enough. It was no longer in the reserves because, in part, it had been used for other purposes such as financing the deficit in the cta cte and the FAE. The IMF was used as a lifeline, which approved a record loan of 50,000 M and later expanded it to 57,000 M. We may never see anything like it.

The outcome is known, the Stand By was used to pay debt that was due and to finance the escape of those who were in pesos and wanted to flee because experience told them that this scheme was not going to work. Such a credit in the end did not serve to pay all the debt that was coming due or to finance the flight of all the holders of assets in pesos. The big mistake of the previous government and the IMF was not to impose at first a regulation of capital flows to order the exit. They thought that with the stocks they would lose the elections and the same thing happened. But they left a catastrophic legacy.

The Agreement as the conclusion of a comprehensive process

As of today, the Agreement with the IMF culminates the difficult process that involved reordering the six main/fronts of inherited external indebtedness.

These fronts are:

1) that of private holders of public debt with the 2020 restructuring,

2) that of debts with private creditors of the provinces with various specific agreements,

3) that of the large private external financial debtors, where thanks to the R 7146 of the BCRA it was possible to refinance 60% of the capital for more than two years,

4) that of the re-profiled holders of the external debt in pesos where, although there is still a relevant amount, it is much less than the inherited and concentrated in two funds

5) that of the Paris Club and the bilateral debt (excluding China) that allowed to postpone payments and take a bridge until the negotiation with the IMF

6) that of the IMF, which with the agreement clears unpayable maturities for 44,000 M that the AM had scheduled for 2021-24.

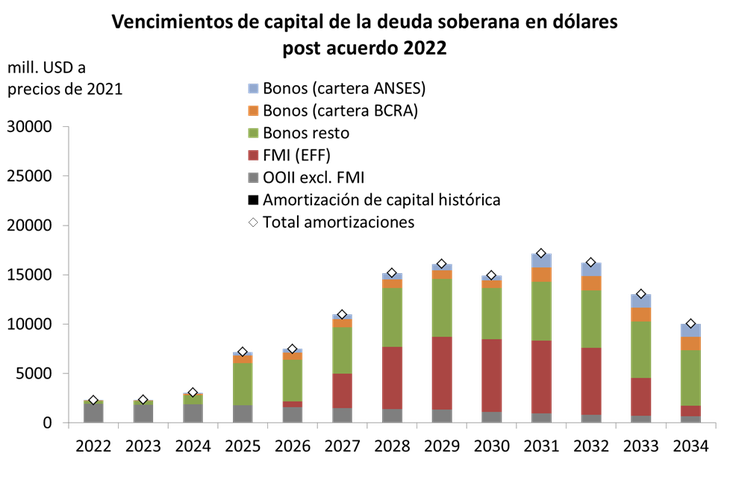

Graph 1 shows what was an insurmountable barrier of external indebtedness in 2020-2023 that had been inherited. Note that it does not include provinces and private maturities.

Renegotiating all six fronts made it possible to flatten and stretch the external payment curve of the Argentine economy from a situation where it was impossible to obtain the dollars to pay and neither was it possible to get creditors to refinance maturities individually.

What the government did was an enormous coordination effort between different financial agents to convince all types of creditors of the will to comply and of the need to make a sustainable time sequence of payments. If the inherited mess was tidied up, everyone could get paid.

The second effort was to convince creditors that in order to pay they need to grow continuously over time. That the recessive adjustments in the end damage the ability to pay.

The advantage in this case is that, if the non-contractive scheme programmed in this Agreement works, the Argentine economy should be much larger in 2027-2034 than in the 2010-2019 average. But the committed payments are lower than those made in that period. Therefore, the Foreign Debt/GDP ratio and the corresponding payments will be sustainable. Which, additionally, will open the doors for the same current private holders to propose extending terms and renewing all or part of the debt that is due.

More important in the short term is that due to its role in the AFI, the agreement with the IMF allows opening new multilateral financing with the World Bank, IDB, CAF and other multilateral banks that need to have this issue resolved. Several of these institutions have already committed significant additional funding. The same will happen with bilateral lenders such as investment banks from various countries that required the Agreement to advance various financings.

The Agreement with the Fund also allows private investment announcements to be made in several fields such as mining, oil and gas, automotive, agribusiness, chemical, tourism, knowledge economy, among others, since in many cases it was a condition of the houses arrays to be up to date with the IMF.

The Agreement has an ambitious objective of accumulation of Reserves at the beginning. This is very important because Reserves are a crucial anchor for a managed float regime. A first boost from the accumulation will be given by the fact that the fund repays the capital payments already made by this government.

On the other hand, the agreement has a very positive element and that is that it recognizes that a devaluation is not necessary as some economists have called for and that it is important to maintain competitiveness at current levels. Accepting an abrupt devaluation would have generated a recession, inflation and little effect on the trade balance or on the financial gap.

The Agreement assumes, at the proposal of Argentina, a strong conviction in promoting exports as the main engine to overcome the external restriction that historically subjected Argentine growth to a frustrating pendulum. Starting from an adequate level of competitiveness measured by the real exchange rate, we will be able to take advantage of export opportunities, but clearly seeking to add more and more value and more links in the chain of the exported good.

Another positive element is that the Agreement will allow stabilizing the reduction in commercial and financial private external debt that we have experienced since 2018. Surely, after four years of net cancellation, the level of use of external financing by private parties is already at levels below those adequate. By normalizing financial relations and having a viable scenario in the rest of the Argentine debts, the largest local companies will find it more accessible to finance investment projects or imports abroad and thus free up local funds for smaller companies.

The Agreement is very innovative in several items compared to the past. First, it does not postulate structural reforms and at the same time recognizes the importance of capital and exchange controls while external and monetary normalization lasts. Surely the accumulation of reserves, an adequate interest rate to remunerate savings in pesos, falling inflation, less excess liquidity, less demand for dollarization, new external financing and new foreign investment will gradually allow restrictions to be relaxed. In these aspects, which, as we have seen, were major mistakes made by the two Stand By, it is more similar to the Agreement implemented by Iceland than to those made with Argentina in 2018 and 2019.

Finally, the Settlement leaves a reasonable inheritance. Some important official of the AM maintained that this scheme is a burden for the next governments. This, in addition to being an irony said by who in 2019 left a payment scheme concentrated in the next government, is false.

The government that starts in 2024 will be able to evaluate how the Agreement worked and will have spent almost its entire term before having to make the first important payment in 2027. Therefore, it will have all the time to see how the Agreement worked and, if they are given conditions, do as Nestor Kirchner did and pay all or part of it. No one imagined in 2003 that it would be possible to cancel everything a few years later. Of course, the debt left by Macri is four times greater.

Even if the next government wanted to propose a new, more contractive Agreement, with pension reform, labor reform or tax laundering, it could go to the future parliament and propose these ideas. That is a great advantage of the Agreement. Whichever sector governs in the future, you will have time to think and evaluate, without the rush of urgent payments to face.

In short, this is an ambitious but realistic deal. It is committed to normalizing the fiscal, monetary, and external spheres and promoting exports and value addition. It does not promote an abrupt and disruptive shock to order the economy from there. These experiments always have a very high social and political cost. It bets on growing continuously and reducing inflation gradually on sound bases, not using magic shortcuts. That is why it was so important in the six years not to have large debt payments and to accumulate reserves. For an economy of the size and potential of Argentina, even in the most conservative growth scenario, payments from 2028 are clearly sustainable.

image.png

BCRA-UNLP-Conicet

Source: Ambito

David William is a talented author who has made a name for himself in the world of writing. He is a professional author who writes on a wide range of topics, from general interest to opinion news. David is currently working as a writer at 24 hours worlds where he brings his unique perspective and in-depth research to his articles, making them both informative and engaging.