The sources stated that the delay in the tender was due to the fact that both the last and current ones are short weeks. Beyond that, the truth is that The BOPREAL series 3 has so far not been attractive to importers as a way to settle debts with its foreign suppliers or with its parent companies. Of the US$3,000 million that the economic team proposed to place in this instrument, in the first four tenders it only obtained US$981 million. That is to say, It still has to channel two thirds of what was planned.

In fact, demand is declining. Even though in mid-March the BCRA It enabled importers with commercial debts prior to the change of government who were not registered in the registry of the AFIP and the Ministry of Commerce to participate in the placements, who until then could not access the bonus. In the two tenders after that decision, only US$100 million and US$89 million were received respectively.

CNV makes the CCL more flexible for importers with BOPREAL

In this framework, the CNV authorities signed this Tuesday general resolution 995, which frees importers who have purchased BOPREAL from the restrictions that weigh on the CCL’s operations to make it more flexible for them to complete the payment to their suppliers. The decision seeks to simplify this mechanism for those who have already acquired the bond in a primary bidding and to support the upcoming BCRA auctions.

Specifically, as of April 1, Importers will be able to operate CCL even if they are leveraged in bonds and will not have to comply with the one-day parking (minimum holding period for the bonds with which the financial dollar is traded) neither the limit amounts nor the prior information regime. This operation without obstacles can be done for up to a magnitude equal to the total nominal value subscribed in the BOPREAL primary tender.

Official sources explained that The objective is for importers to be able to settle via CCL without restrictions the difference that is generated between the value of the debt with their suppliers and the foreign exchange they obtain when they dispose of the BOPREAL in the secondary market.. As the BOPREAL is quoted at a parity of less than 100% (which varies according to each series), when the importer sells the bond on the market to settle the liability with its creditor before the title matures, it receives less money. For example, if you sold it for $70 for every $100 of face value, you could now pay off the remaining $30 without the obstacles that weigh on cash with liquid.

This rule is complementary to two other measures that the CNV itself and the BCRA had taken some time ago: the one that freed BOPREAL itself from the restrictions on exchange operations in the capital market and the one that excluded importers from the official market who have operated on CCL.

Although, as Ámbito anticipated, the economic team has already defined the set of restrictions on financial dollars that it will remove when the Government decides to move forward with lifting the stocks, for the moment they will remain in force. The exception, for now, only applies to these operations associated with BOPREAL.

BOPREAL series 3: the reasons for low demand

Despite the low appetite of importers for series 3 of the BOPREAL, official sources assure that “the result of these tenders is not of concern” and they argue that it is only “an alternative” for companies.

In any case, BOPREAL was proposed by the economic team as an important piece of its transition strategy at the monetary, exchange and reserves level. This is the bond for importers with commercial debts prior to December 12, which is subscribed with pesos but is denominated in dollars and which aims at several fronts at the same time: it was designed to decompress the situation of liabilities for imports (which also continue growing due to the staggered payment system implemented by the current administration), to aspire pesos, to dollarize a portion of the remunerated liabilities and to take pressure off the parallel dollar.

In series 1 and series 2, the BCRA exhausted two quotas of US$5,000 million and US$2,000 million. For the third, a target amount of US$3,000 million was set, but the tenders are progressing in dribs and drabs.

For what is this? As Ámbito had anticipated, The characteristics of the 3 series make it less attractive than the previous ones for importers. The bonds of this series are authorized for transfer and negotiation in the secondary market, accrue interest at a nominal annual rate of 3% and amortize in three quarterly installments, from November 2025 to May 2026. But, according to the operators, there are two factors of its structure that work against it: on the one hand, it has longer amortization periods than series 2 (which has received foreign exchange flow since the middle of this year) and, on the other, it does not include the tax benefits that the first (which did not pay PAIS tax and can be used to cancel obligations with the AFIP).

Furthermore, there was another factor that made him less attractive: the compression of the exchange gap. The fall of the cash with settlement (CCL) during February and the subsequent stabilization below $1,100 in recent weeks (driven by the supply in the cash with settlement market generated by the blend dollar for exporters and the lack of demand due to the liquefaction of the economy’s pesos) made it eventually more convenient for importers to buy CCL To settle their debts they have to subscribe to series 3 of the BOPREAL and download the title on the secondary market.

According to calculations by Salvador Vitelli, head of research at Romano Group, in the four series 3 tenders, the implicit exchange rate that importers accessed through BOPREAL to settle debts with their suppliers was on average 30% higher than the CCL value.

In that sense, some sources told this medium that in recent weeks There were companies that took advantage of the reduction in the gap and turned to financial dollars to cancel liabilities with their suppliers. from abroad, despite the cross restrictions that exist to access the official dollar if CCL is operated. Other firms, however, say that they continue to have problems to regularize their situation, such as the automotive company General Motors, which suspended production at its Santa Fe plant for two weeks and cited “inconveniences with the supply of parts from suppliers affected by payments abroad.”

BOPREAL and commercial debt

Outside of the large stock of inherited commercial debt, which grew strongly in 2023 in a context of foreign currency shortages exacerbated by the drought, the truth is that liabilities for new imports arranged as of December 13 continued to grow.

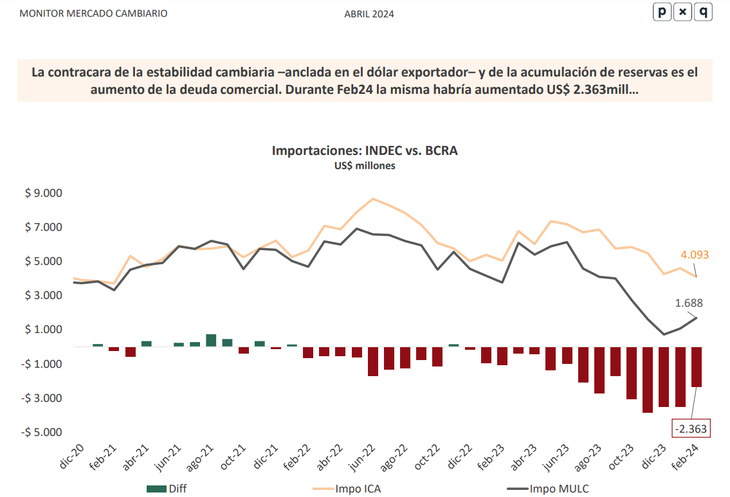

As Ámbito said, Between December and February, import payments reached nearly US$9.4 billion, an amount that far exceeds the US$7,491 million channeled via BOPREAL in the same period. This is because the BCRA established that new purchases abroad would have a scheme of staggered access to the official dollar for their cancellation, which in most products is four installments of 25% each.

image.png

This opened a four-month window that allowed the Central Bank to go through the summer with net foreign currency purchases of about US$8,526 million between December 11 and February 29. However, foreign currency purchases were lower than the new commercial debt generated. This implies that, Without stepping on the payment of imports, there would not have been a recovery of international reserves.

In December, barely 17% of imports were paid; in January, 23%; and in February, 41%. From now on, the staggering defined by the BCRA indicates that the percentage would continue to grow in the future until the gap between purchases and payments is closed. Thus, a report from the consulting firm PxQdirected by Emmanuel Álvarez Agis, pointed out that the new commercial debt generated is the other side of exchange stability and the recovery of reserves, and “implies a challenge in the coming months, when import payments become normal.”

In this regard, PxQ estimated that between December and February the stock of commercial debt remained practically stable at around US$51,000 million, if for the second month of 2024 some US$34,000 million of inherited debt are still considered. pending, plus US$9,395 million of new liabilities for imports and the slightly more than US$7,000 million channeled via BOPREAL.

“In this sense, the BOPREAL tenders would seem to serve as an instrument to absorb a potential demand for dollars rather than to resolve the commercial debt accumulated until the new management took office,” PxQ concluded.

Source: Ambito