“The company of semiconductors with the greatest capitalization of the world is making a solid case that its business will accelerate from this point, despite the fact that the market consensus still fears a slowdown,” said its analysts. The latest quarterly results reinforced that vision, says the bank: “Solid gross margins, revenues excluding China on the rise and recovery in networks” and were some of the bank’s positive comments about the expansion of the Nvidia supply chain.

And although Nvidia offered little orientation on the second half of 2024 and the year 2026 – a caution attributed to geopolitical sensitivity around the commercial warfare – Morgan Stanley believes that the underlying demand remains strong and that the current bottlenecks in the racks, which have generated an increase in inventory between original design manufacturers (ODM) soon.

Nvidia under the magnifying glass of experts

In this regard, the investment advisor, Gastón Lentinihe comments in statements to this media that “Nvidia is one of the most thriving companies and, at the same time, more volatile in the current market.” And he explains that until last year, the S&P 500 giant had very high profitability margins, around 55-60%.

However, after the imposition of tariffs during the presidency of Trump and the resurgence of the commercial war, their margins were significantly reduced. “In the results of the first quarter of 2025, it reported a margin of 42%, which was one of the main factors that explain the strong decline in the price of its action: it went from worth $ S153 au $ S87, a fall close to 40%,” Lentini recalls.

This collapse generated an important restriction for many investors, since “not all are willing to tolerate that level of volatility,” he says. However, from that floor there was a very significant recovery. Today the action quotes around US $142, which implies a 65% rise from its lowest point.

For its part, Paulino SeoaneHead Investment Ideas in Balanz Capital, indicates that Nvidia surprised by seventh consecutive quarter with better results than expected, both in billing and profits, In line with what Lentini raises. The company reported revenues for US $ 42,000 million in the quarter, despite the impact of the prohibition of selling its H20 chip to China, which subtracted about US $ 10,000 million in sales.

“Even so, it maintains a strong rhythm of expansion: it grew 69% year -on -year after having advanced 270% the previous year. Some analysts see in this deceleration a sign of convergence towards more sustainable growth rates, especially when considering that its stock market valuation already reaches US $ 3,3 billion,” says Seoane.

NVIDIA 1.JPG

And he adds that the gross operation margin is 60% and the P/E multiple in the area of 30, which places it in the lower range of the range for such a company. “In case all this were not enough, a new ‘player’ appears in the demand for the sovereign governments, both India and the Saudis want to build their own industrial parks of AI so as not to give in all this to third parties,” warns Balanz’s strategist.

Buy, sell or maintain

For Lentini, the big question is now: “Nvidia is expensive or cheap? “In your opinion, at these prices it is not time to buy. Why? Because, beyond Nvidia, it is a leader in its sector, it has no debt and maintains sustained growth in your sales, the global context is complex.” Commercial tensions have not been resolved and that represents a risk for your business, “says Lentini.

For its part, Seoane believes that although Nvidia surpassed Microsoft as the most valuable company in the world, “I still do not reach its historical maximums, although it is close.” Without a doubt, a company that invoice US $ 42 billion in a quarter, has a gross margin of +60% and grows sustainand also offers a cuasi monopoly product with low multiples, it must be on any medium and long term portfolio. “The risk, of course, is more geopolitical and regulatory than anything else,” says the expert.

It should also be remembered that NVIDIA has customers to the Top 10 of the companies of the S&P 500 (that is, 40% of the US Market Cap ‘). It is enough to see the capital expenses (CAPEX) of these companies in AI for the coming years and This is Nvidia’s entryconcludes Seoane.

Thus, although many technical and fundamental indicators could suggest a purchase opportunity, analysts agree to opt for prudence. “Whoever decides to invest in these levels must do so with full awareness that volatility will continue to present.” In my case, I would expect a correction to consider a more favorable entry, ideally around US $120, or even better close to US $ 15, “Lentini concludes.

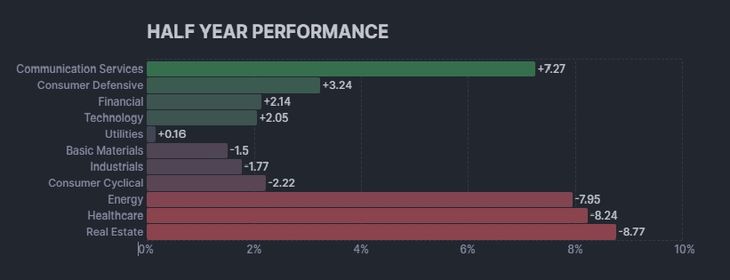

The performance of the technological sector on Wall Street

Matías Waitzelpartner of At investorsanalyze in dialogue with this medium that, the technological sector had a moderate year start. “Nasdaq 100 accumulates a rise close to +3% so far from 2025, and is below sectors such as Energy and finance. However, the panorama remains promising, with solid foundations promoted by the advance of artificial intelligenceCloud Computing and Global Digital Transformation, “says the specialist.

Tech.jpg sector

And, according to projections of Deloittetechnology spending would grow a 6.5% this yearwhich could translate into a new stage of expansion for large technological ones. “Personally, in addition to positioning myself in the QQQ index ( Ticker of the ETF that follows the performance of the Nasdaq-100 index) I like the following companies:

- Google (Googl): Solid in advertising, AI and Cloud; With attractive valuation.

- Apple (AAPL): Resilience and user loyalty; Strong bet in services and Ia.

- Microsoft (MSFT): Leader in Business Solutions and IA, with robust balances.

Together with Nvidia, the actions of Google (Googl), Apple (AAPL) and Microsoft (MSFT) make up the top 5 of the world’s most valuable companies for market capitalization. Google stands out for its strength in digital advertising, its growing presence in artificial intelligence and cloud services, all with a valuation that remains attractive to investors. Apple combines the resilience of your business with a base of faithful users, while deepening its strategy in digital services and IA -based technology. For its part, Microsoft leads in business solutions and development of AI, backed by solid balances and an enviable financial position.

Source: Ambito

I am a 24-year-old writer and journalist who has been working in the news industry for the past two years. I write primarily about market news, so if you’re looking for insights into what’s going on in the stock market or economic indicators, you’ve come to the right place. I also dabble in writing articles on lifestyle trends and pop culture news.