Before becoming the new Minister of the Interior, Guillermo Francoshad predicted an official dollar between $600 and $650, which he had described as “reasonable”. Then they assumed Javier Milei as president and Luis Caputo as minister of economy, and They raised the official dollar to $800 (which implied a rise of 118%). However, in less than two months of management, that competitiveness gained has already lost 25% and precisely The multilateral real exchange rate (TCRM) is already below what the official projected.

“The December dollar of $800 lagged behind inflation and is below the Franc dollar of $650. On December 13 it was at $800 and currently it is at the level of $604”the economist published this Monday, Amilcar Collante on the social network X (ex Twitter). The fact is that the inflationary inertia after the devaluation was very strong: The CPI for December stood at 25.5% monthly and analysts project that January will be around 20%.

Competitiveness: how does the dollar reach the harvest?

For Walter MoralesPresident of Wise Capital, The market today does not see an imminent devaluation, although it does see an acceleration starting in March. According to the futures on Matba-Rofex, 2% crawling peg would continue through Februaryfor later accelerate to 8% during March and 15% in April. Which implies a projection of a wholesale dollar of $1,063 at the end of April. For Morales, “it is reasonable to have a competitive dollar before the liquidation of the thick crop begins.”

“The problem with adjusting the wholesale dollar 2% in February, 10% in March and 15% in April is that would return to a real exchange rate similar to that obtained the day after the adjustment made by Massa. Without a doubt, it can become a dollar that do not tempt the field to liquidate soybeans starting in May“said the analyst.

Given this, it is important to analyze How the BCRA reserves will arrive in the second quarter of the year.

According to the same analysis, “until the soybean liquidations come in, you need to have a trade surplus equal to or greater than au$s1,000 million. December was US$1,018 million, ergo, if placed 100% of BOPREAL dollar needs will begin to decline towards May and with it the exchange rate gap, although this last point also plays a role in having a successful fiscal anchor.”

In this regard, it is important to highlight that the Minister of Economy, Luis Caputoannounced on Friday the reverse of the fiscal chapter of the Omnibus Law. Fairly This section included changes in withholdings, retirements, money laundering, moratorium, Income Tax and Personal Assets. According to private measurements, this is equivalent to 1.8% of GDP and puts in check the fiscal anchor with which the Government seeks to moderate inflation.

Reserves, BOPREAL and BCRA accounts

image.png

Right now, the net reserves of the Central Bank (BCRA) are currently located around negative US$7.1 billion. It should be noted that the minimum level was marked on December 13 with negative US$11.3 billion. “It accumulates a rise of US$4.2 billion in 45 days”estimated Salvador VitelliHead of Research Roman Group.

But beyond recovering reserves, The BCRA had two other important sources of fire, on the one hand the debt with importers and, on the other, the remunerated liabilities. Regarding the first, it is worth highlighting that the last tender for the Bonds for the Reconstruction of a Free Argentina (BOPREAL) by the Central Bank was successful and managed to place almost US$2.5 billion.

“The high adhesion in the BOPREAL Series 1 tender, characterized by its financial complexity and expiration in 2027, evidenced increasing demand for some reasons: The rise of the Dollar Cashed with Settlement (CCL) increased the attractiveness of BOPREAL for importers, allowing them to sell it against dollars and cancel debts without losing access to the official exchange rate and an exchange rate of around 1,280 pesos. Furthermore, the increase in the volume operated in the secondary market,” explained the economist Elena Alonso.

image.png

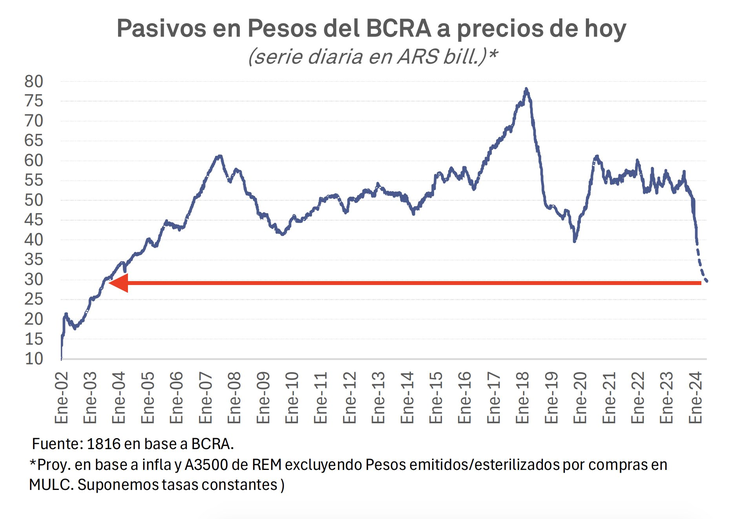

Regarding the second point, passive passes, it seems that the path to “liquify” the debt would take place sooner than expected. According to a calculation of the 1816 consultantof maintaining the passive repo rate and using projected inflation by the REM of the BCRA By the end of May, liabilities at constant prices would fall to 2003 levels.

Source: Ambito

I am a 24-year-old writer and journalist who has been working in the news industry for the past two years. I write primarily about market news, so if you’re looking for insights into what’s going on in the stock market or economic indicators, you’ve come to the right place. I also dabble in writing articles on lifestyle trends and pop culture news.