Luis Caputo wants banks to start setting the rates of fixed terms and remunerated accounts based on the returns of the LECAP instead of those of the repos. Why isn’t that happening yet?

The Government wants banks to modify the way they set the interest rates they pay to their clients for fixed terms. The official intention is that the reference stops being the monetary policy rate (that of the overnight repos issued by the Central Bank) and becomes the yield of the LECAP, the short bills issued by the Treasury. However, this did not begin to materialize. In the market, they warn that there are two factors that, for the moment, are blocking this change.

The idea of the economic team is in tune with the policy of accelerating the dismantling of the stock of remunerated liabilities of the BCRA and its replacement with Treasury debt, which it strongly encouraged in May. In that train, the Ministry of Economy activated a biweekly bidding calendar, which includes the placement of short letters at a fixed rate, the LECAP.

This is the instrument chosen for banks to migrate their repo holdings. Thus, last month the stock of BCRA liabilities was reduced considerably and, in fact, ended at its lowest level since 2004 measured in real terms. The other side, as Ámbito said, was a record monthly net debt for the Treasury of $11.9 trillion (3.4% of GDP, according to Facimex) and a greater accumulation of short-term maturities.

The other objective behind the creation of a short peso yield curve issued by the Treasury is the change of reference for setting banks’ deposit rates: those for fixed terms and remunerated accounts. This is what he himself stated a few days ago. Luis Caputo during his presentation at the IAEF congress. He said that the BCRA repo rate will become “almost nominal” and He asked that banks begin to take the performance of the LECAP as a yardstick placed by the Ministry of Finance.

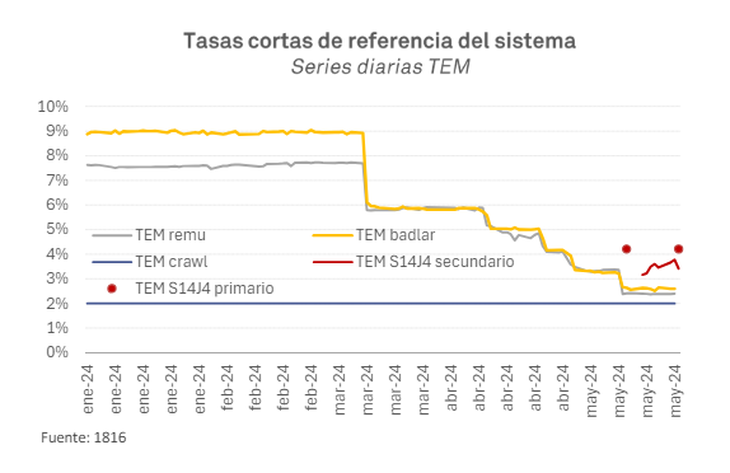

But This is not corroborated in practice at the moment. The BADLAR rate (the average of what banks pay for deposits to fixed term over $1 million) moved practically in mirror with the successive reductions in the monetary policy rate that the Central Office applied since it assumed the current management within the framework of the blender plan. And after the latest measures of the economic team, which accelerated the disarmament of the passes, it hardly moved. Today it is around 2.6% monthly, a few tenths below the 3.3% paid for one-day passes. Remunerated accounts rank even a little lower.

image.png

Reference change in rates: the obstacles that the market warns

The consultant 1816one of the most read at the tables of the City of Buenos Aires, pointed out that The rates of fixed terms and remunerated accounts “continue to be determined mainly by the repo rate”. And he warned that there are two factors that explain why banks do not leave that reference behind.

- On the one hand, the Ministry of Economy limits the issuance amounts of the LECAP in their tenders. There was a cap of $10 billion in the first auction in May and one of $3.5 billion in the second, of which only $1.5 billion came out with a predetermined minimum rate.

- On the other hand, the regulatory change issued last month (through communication “A” 8020) clears the limit of financing to the Treasury that the banks have according to their “historical repo position”, but “does not ensure that new deposits can be placed in Treasury debt” without exceeding said limit. Furthermore, it does not exempt LECAPs purchased on the secondary market from this limit, but only those acquired in primary bidding.

“As long as this is not changed (especially the issue cap), the repo rate will continue to be the marginal rate of the system, and therefore the reference for setting deposit rates,” stated the last report from 1816. And it considered that, At least until the conditions for the next tender are announced in two weeks, this will continue to be the case.

Source: Ambito

I am a 24-year-old writer and journalist who has been working in the news industry for the past two years. I write primarily about market news, so if you’re looking for insights into what’s going on in the stock market or economic indicators, you’ve come to the right place. I also dabble in writing articles on lifestyle trends and pop culture news.